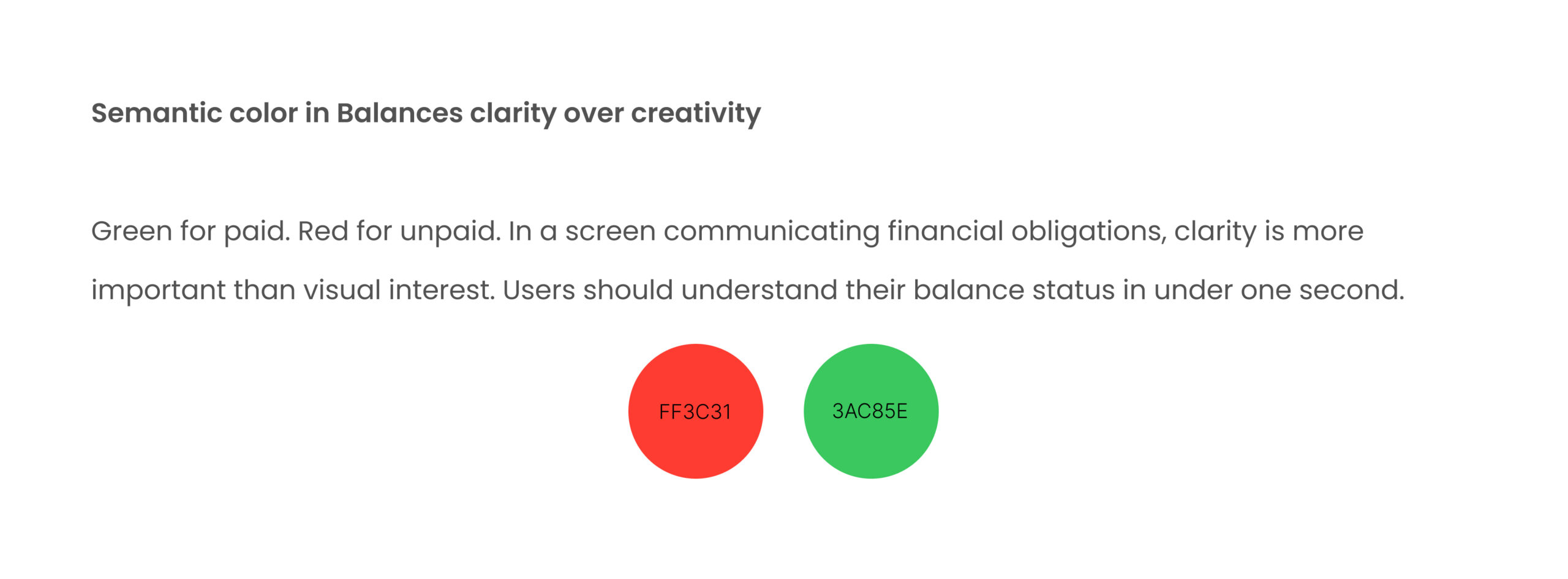

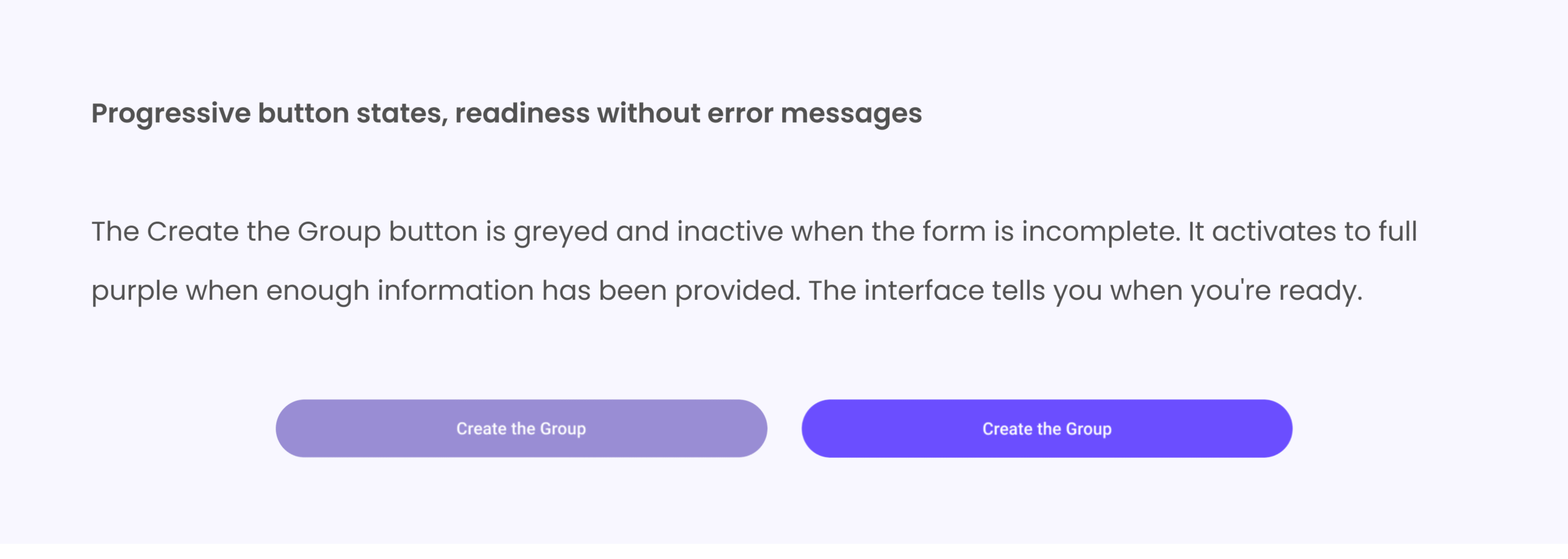

The product design lead didn't agree with my animation. I proved him wrong with usability testing.

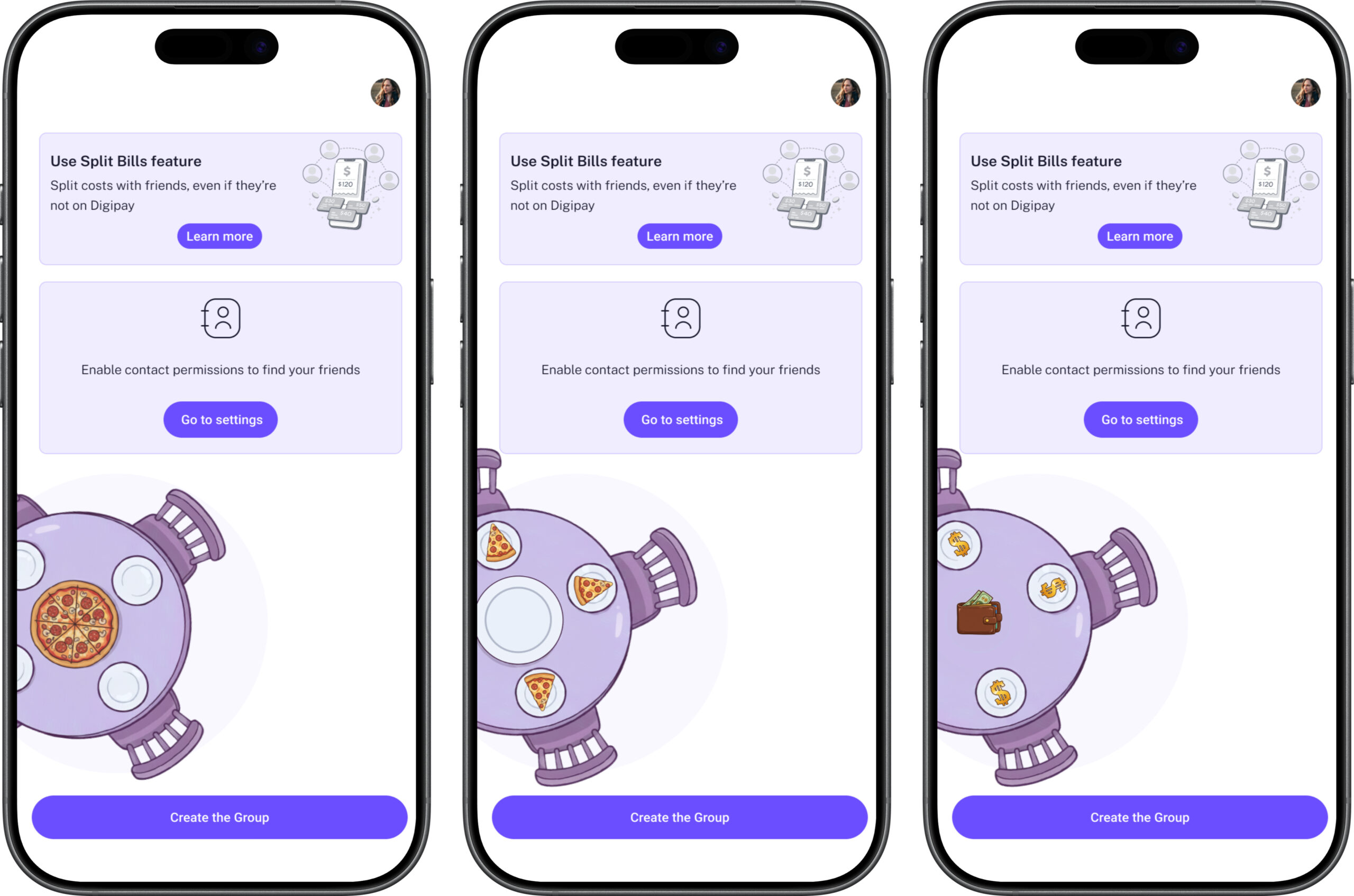

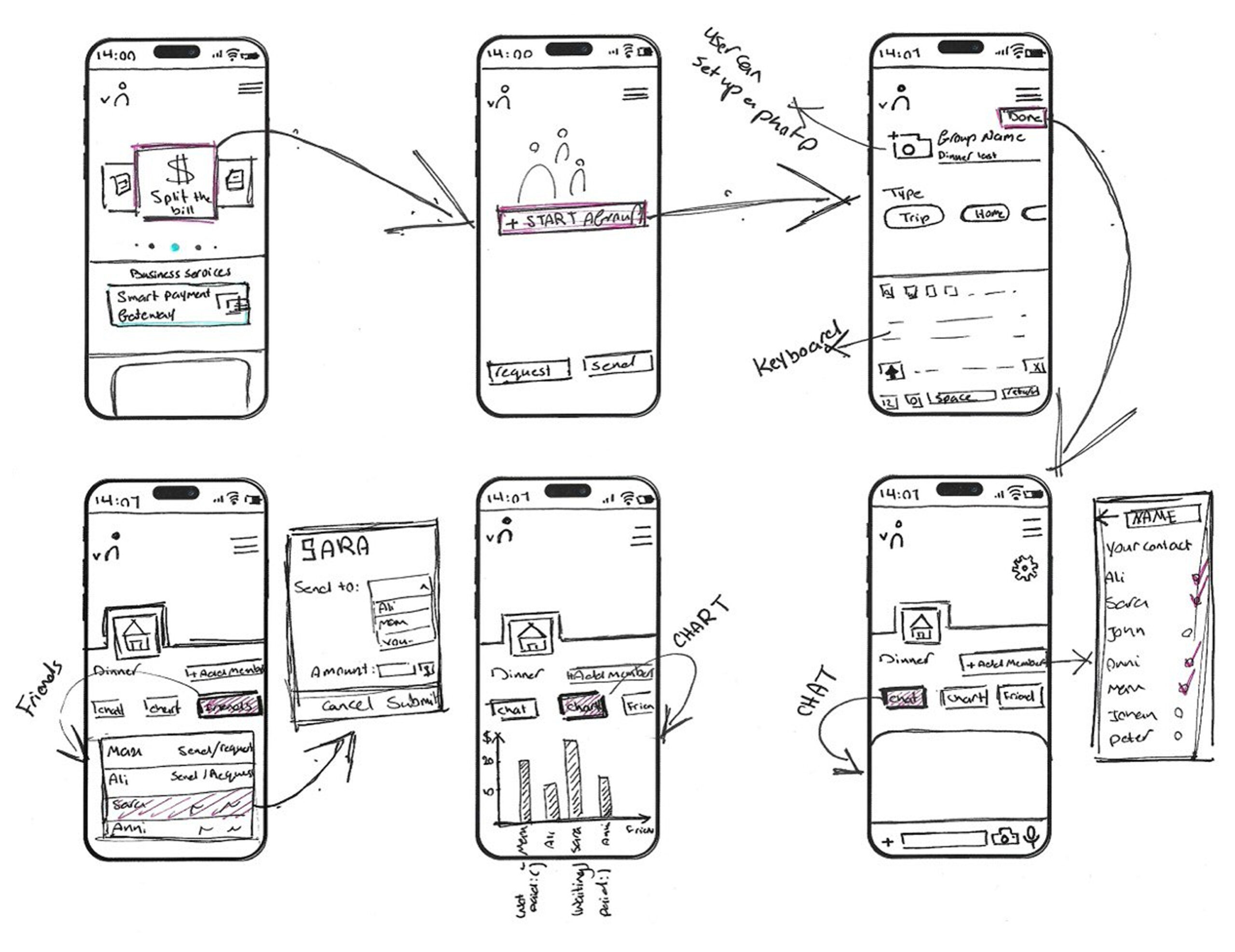

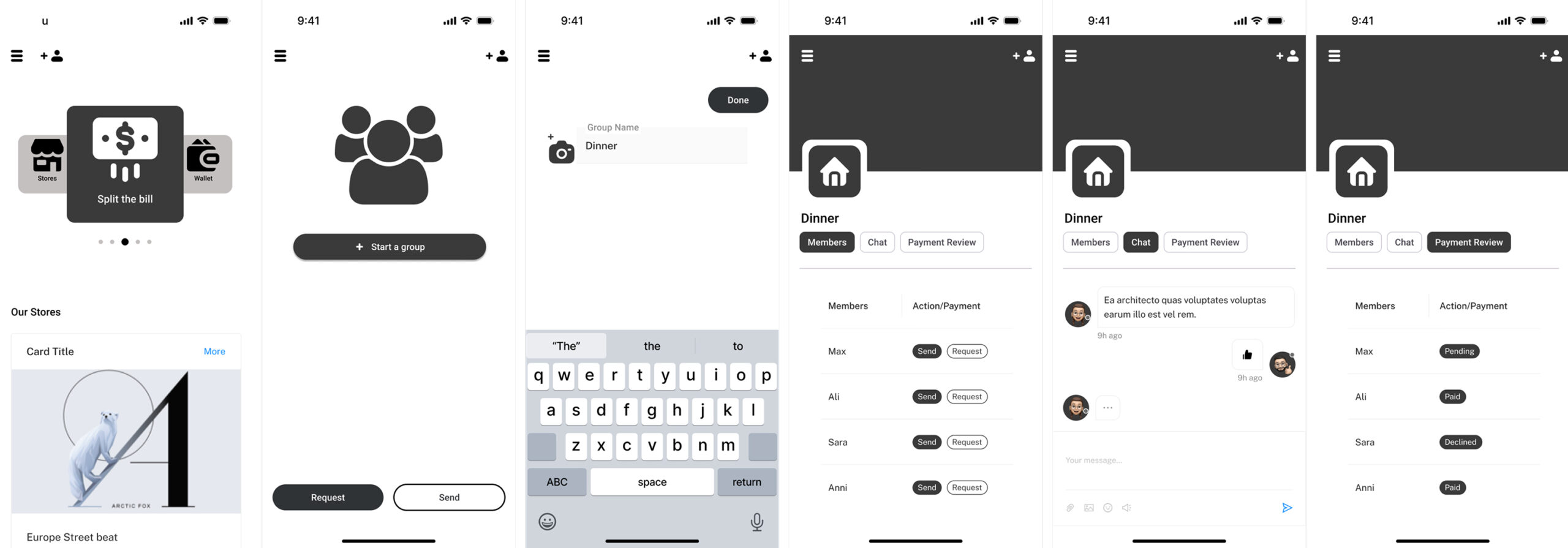

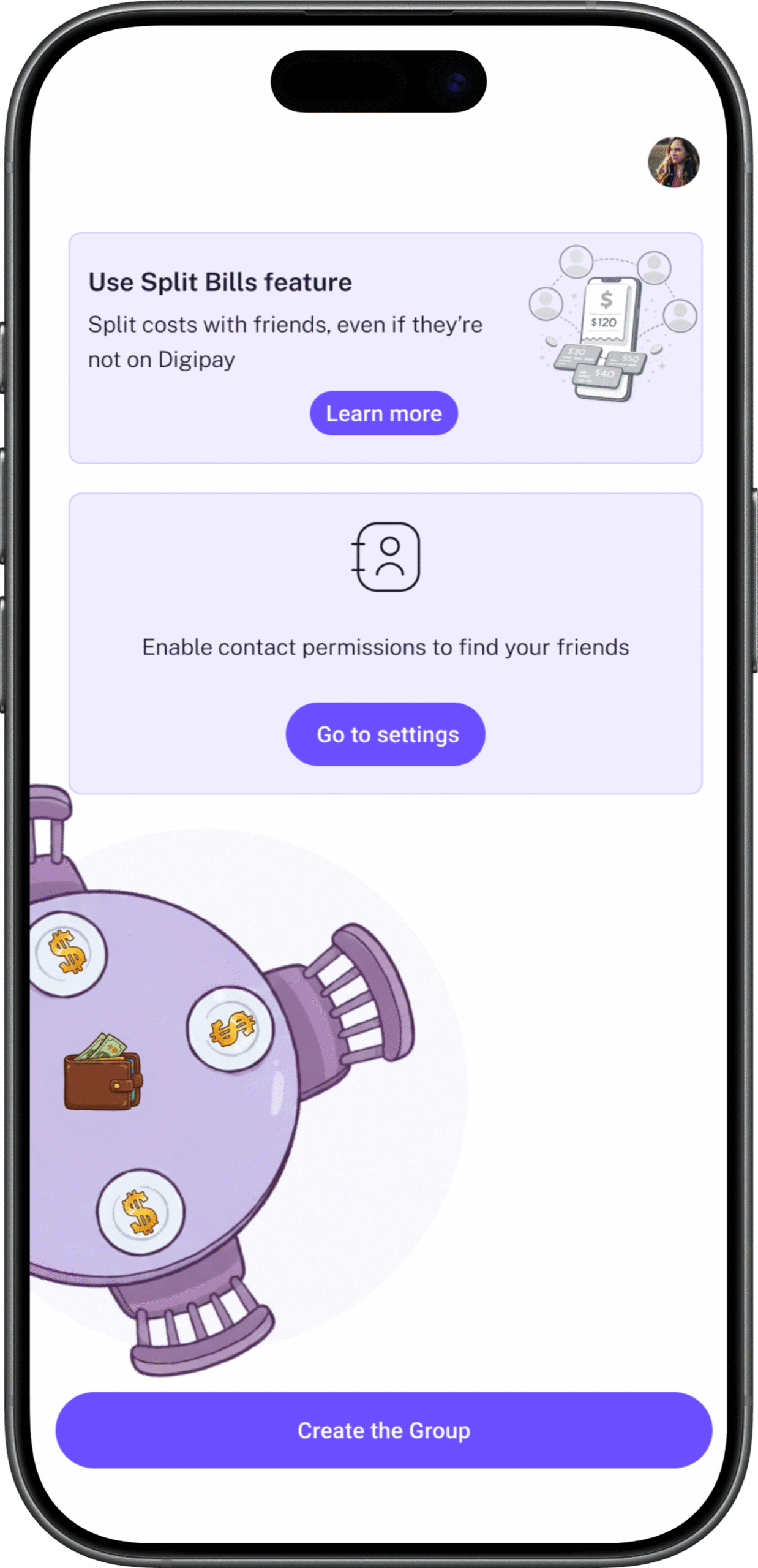

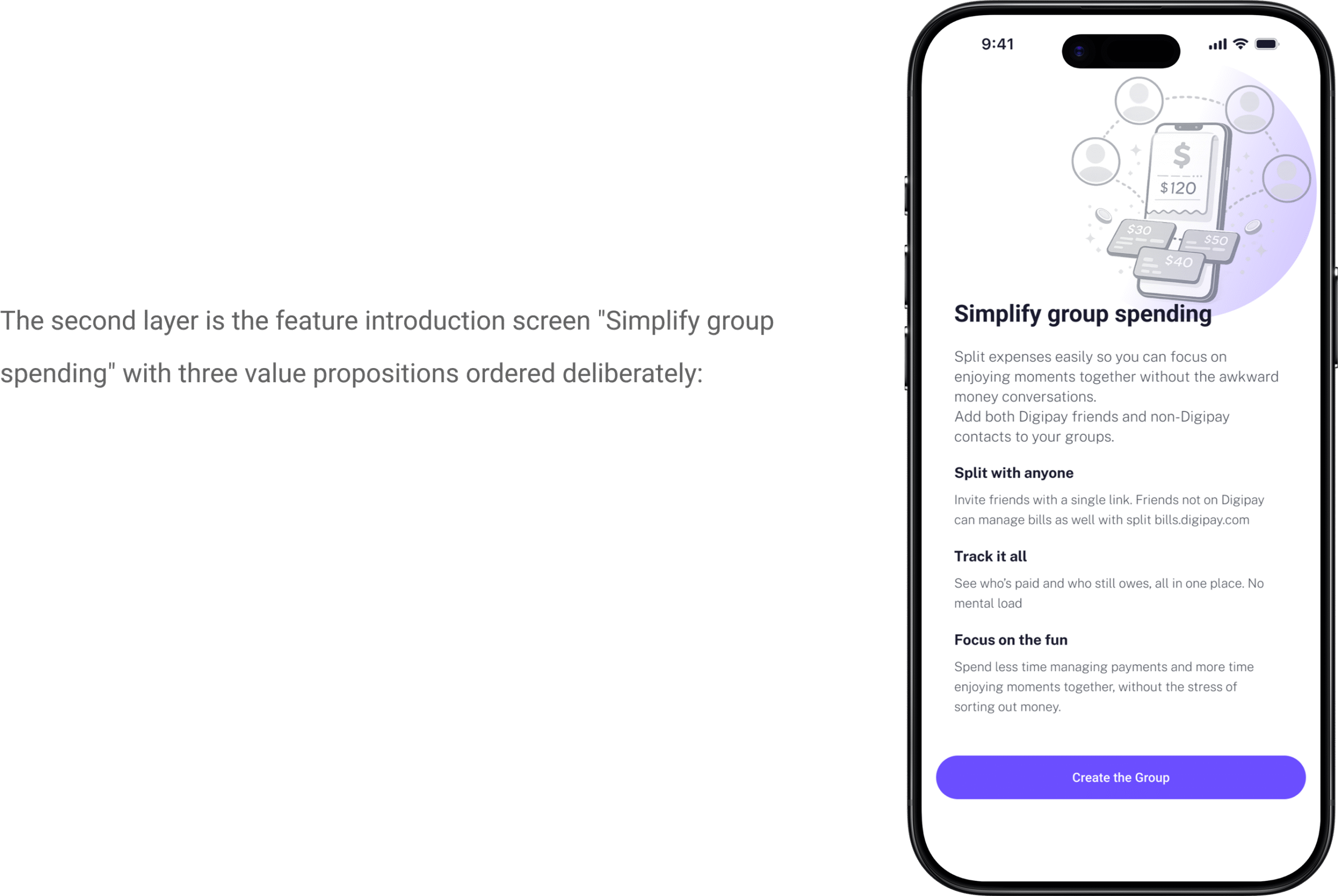

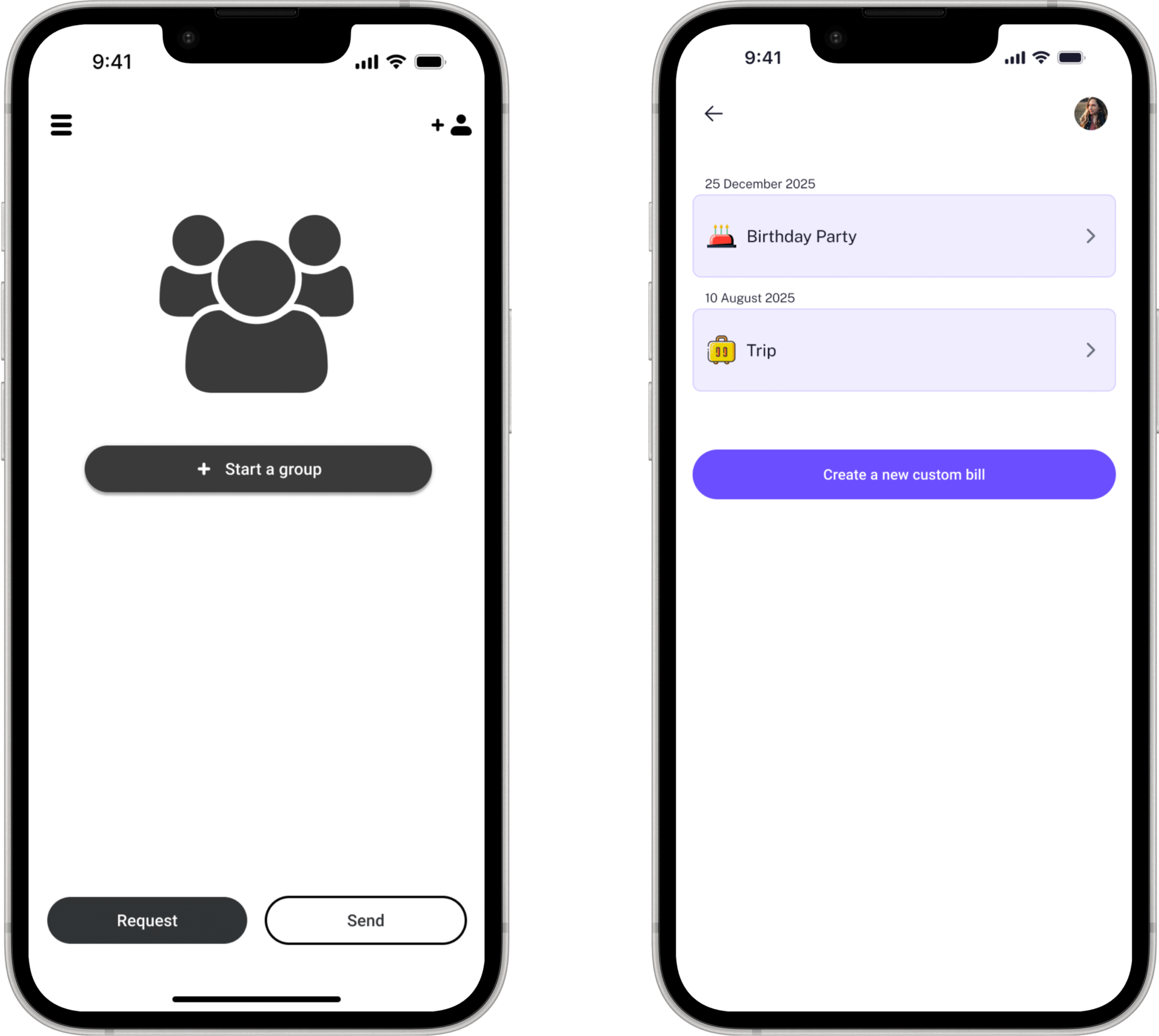

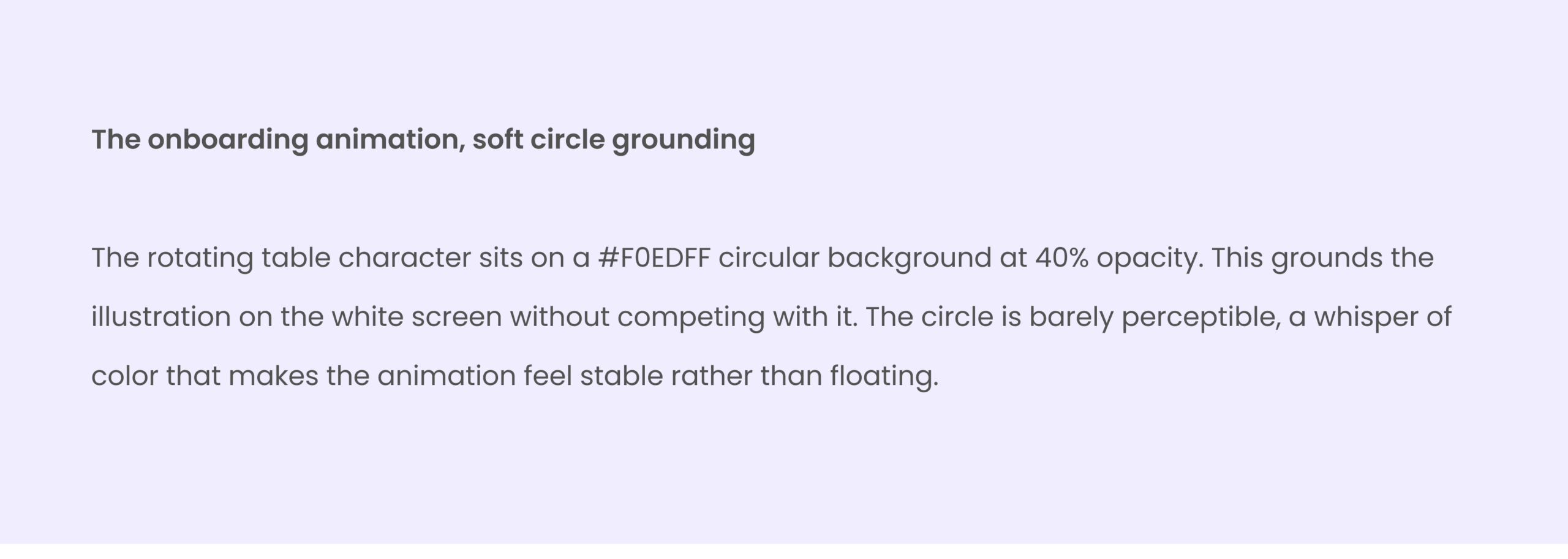

The onboarding animation I designed, a rotating table with pizza slices appearing on individual plates, each person taking their portion, the bill settling in the centre, was rejected in the first review. The product design lead felt it was unnecessary, potentially confusing, and that a new feature should communicate through straightforward text and static illustration rather than animation.

I understood his position. But I had a specific reason to push back.

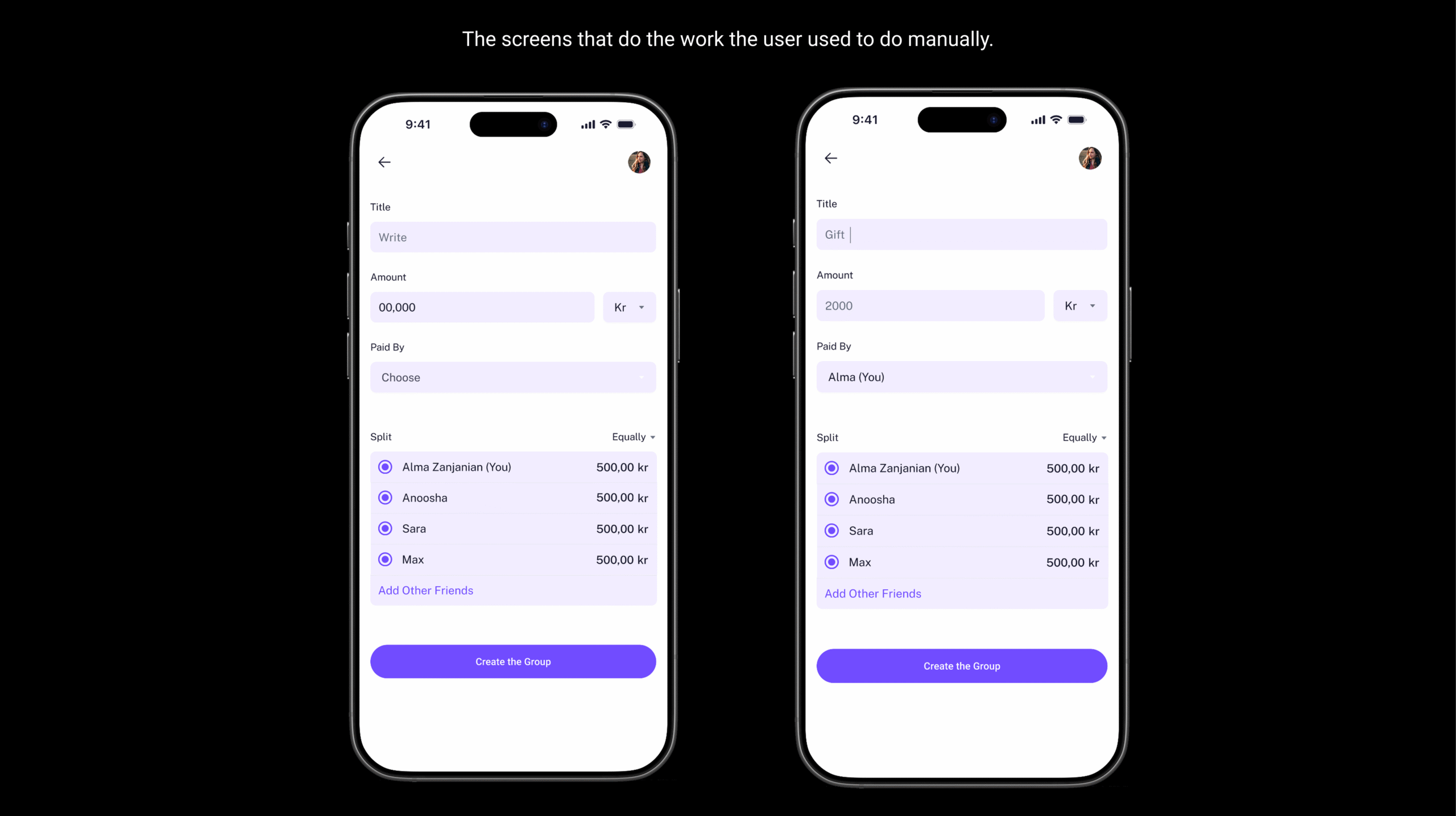

Because no user in our research base had ever used a split bills feature inside a fintech app, the first seconds of onboarding were carrying critical weight. Users needed to understand the concept immediately and intuitively, not just read and comprehend, but feel what the feature was for before a single word of explanation.

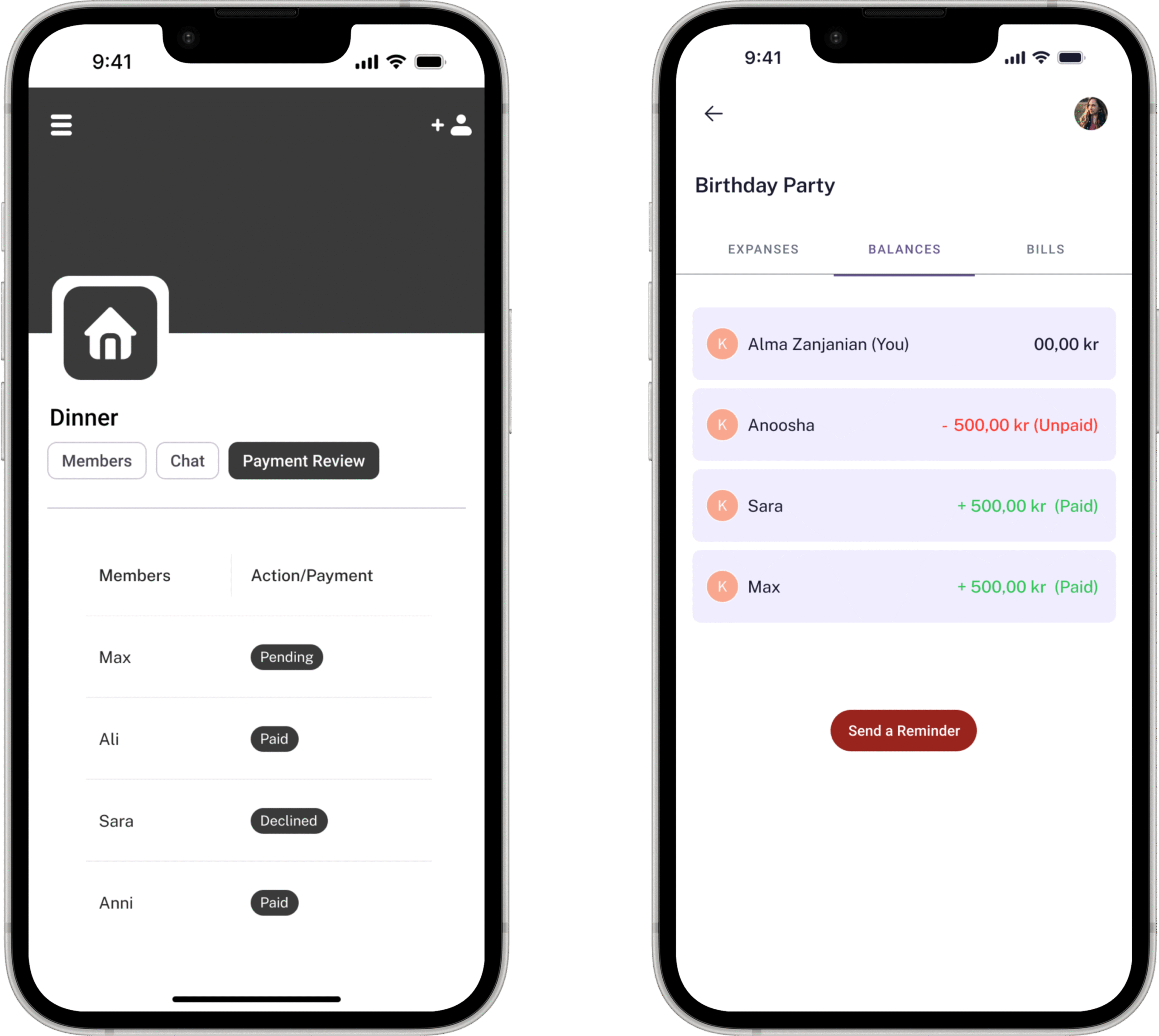

The animation tells a complete story without words: people gather, food is shared, each person has their portion, the bill is divided and settled. A full social and financial narrative in a few seconds of motion.

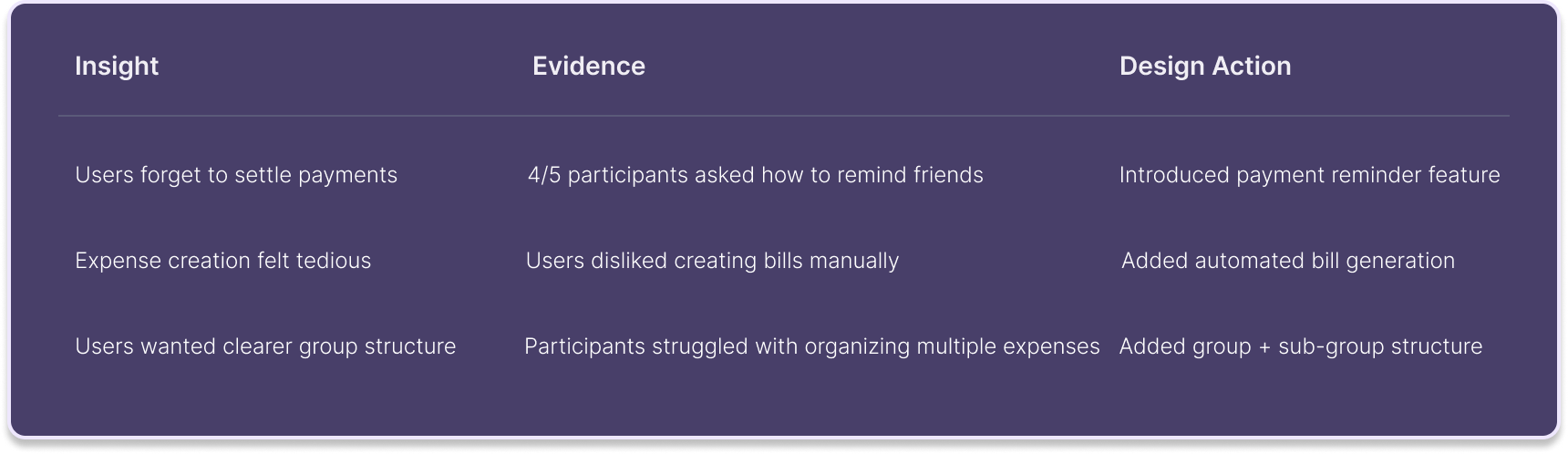

I structured usability testing questions specifically around comprehension, did participants understand what the feature was for before reading any text? The results were unambiguous. Participants who experienced the animation understood the concept immediately. Several smiled instinctively when it played the exact emotional register I was designing for. Something that felt light and social, not transactional.

The product design lead reviewed the testing evidence. The animation stayed.